Many people want to start building wealth, but feel overwhelmed by questions like:

- “How much should I save?”

- “Should I invest?”

- “How do I balance risk and security?”

- “Where should my money actually go?”

If that sounds familiar, you’re not alone.

Asset building does not start with complicated investing strategies.

It starts with understanding your money clearly.

Once you organize your finances into categories, it becomes much easier to see:

- what you already have,

- what you need,

- and how much risk you can realistically take.

This article introduces a simple 4-step approach to help beginners start building assets with more confidence.

Step 1: Understand What You Own

Before investing or growing your assets, it’s important to understand your current financial situation.

Start by listing:

- Savings

- Investments

- Insurance

- Cash

- Property

- Loans

- Credit card debt

- Mortgages

In simple terms:

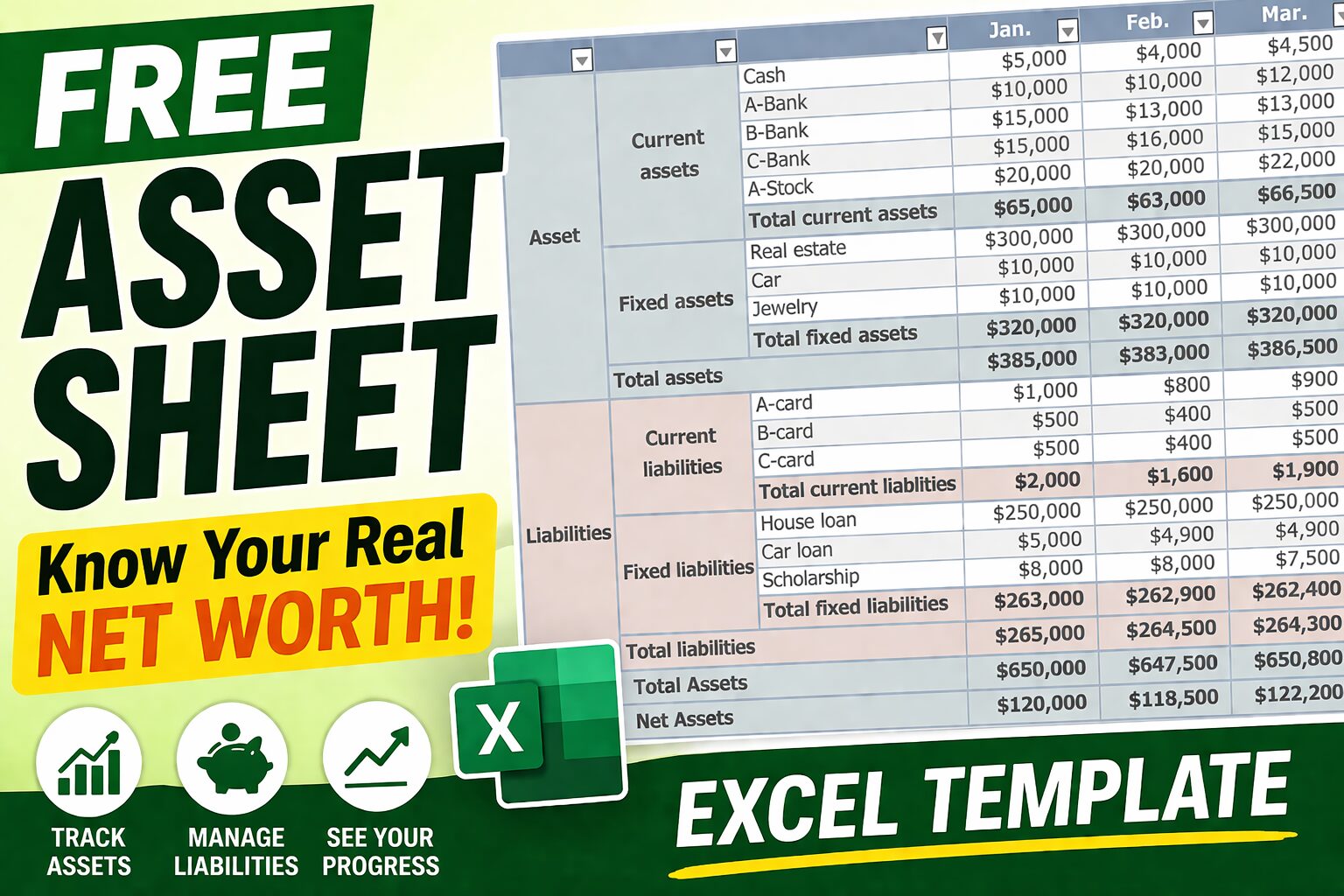

Net Worth = Assets − Liabilities

Knowing your net worth helps you understand where you stand financially today.

Types of Assets

Current Assets

Money or assets that can easily become cash within one year.

Examples:

- Savings accounts

- Cash

- Stocks

- Investment funds

Fixed Assets

Assets held for longer periods.

Examples:

- Real estate

- Cars

- Jewelry

- Valuable items

Types of Liabilities

Current Liabilities

Debt that must be repaid within one year.

Examples:

- Credit card balances

- Unpaid bills

- Taxes

Long-Term Liabilities

Debt repaid over many years.

Examples:

- Mortgages

- Car loans

- Student loans

-

-

【Free Excel Asset Sheet】Track Your Net Worth & See Your Financial Reality Clearly

Do you feel unsure about your financial situation—even if you’re saving money? You’re not alone. Many people: But still feel anxious about money. The reason ...

Step 2: Understand Your Monthly Living Costs

Before deciding how much to invest, you need to know:

“How much money do I actually need to live?”

Using a household budget or expense tracker can help you understand your monthly spending habits.

Common categories include:

- Food

- Utilities

- Rent or mortgage

- Insurance

- Transportation

- Communication

- Education

- Medical expenses

- Entertainment

This step creates the foundation for stable asset management.

Because if you don’t know your monthly costs, it becomes difficult to judge how much risk you can safely take.

-

-

Best Kakeibo Templates (2026) | Find the Right Budget for You

“Which budget template should I choose?” If you’ve ever felt overwhelmed by too many options, you’re not alone. In this guide, you’ll find a clear ...

Step 3: Prepare for Special Expenses

Not all expenses happen every month.

Some large expenses appear only occasionally, such as:

- Car purchases

- Home down payments

- Education costs

- Travel

- Moving expenses

- Emergency repairs

These are often called special expenses.

Preparing for them separately can help prevent financial stress later.

A helpful approach is to estimate:

- how much money you’ll need,

- and when you’ll need it.

This makes saving more intentional and realistic.

-

-

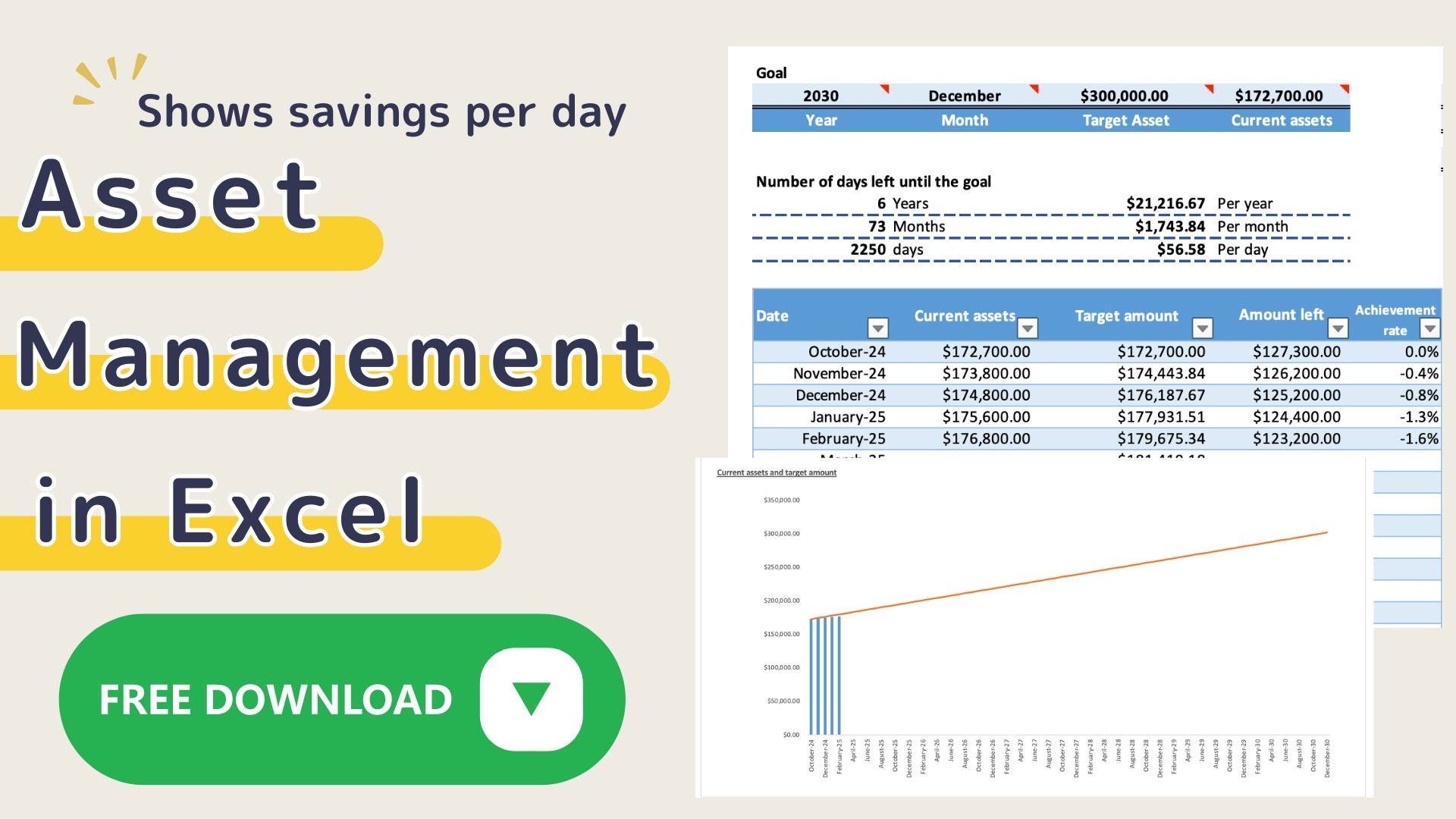

Visualize Your Annual Expenses| Stop “Unexpected Spending” Before It Happens

“Why is there so little money left this month…?” Even if you’re tracking your budget,you may still feel this way. But the problem isn’t your ...

Step 4: Categorize Your Money

Once you understand your finances, the next step is organizing your money by purpose.

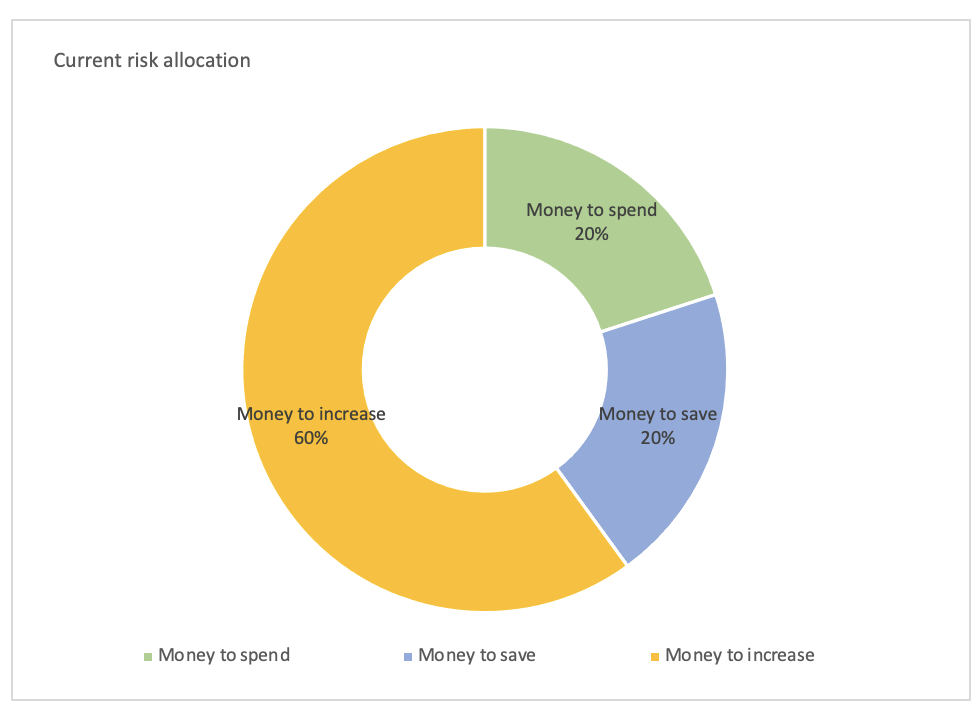

A simple approach is dividing money into three categories:

| Category | Purpose |

|---|---|

| Money to Spend | Everyday living and emergencies |

| Money to Save | Medium-term goals and planned expenses |

| Money to Grow | Long-term investing and wealth building |

1. Money to Spend

This is money that needs to stay safe and accessible.

Examples:

- Emergency savings

- Living expenses

- Cash reserves

A common recommendation is:

Keep 3–6 months of living expenses available.

2. Money to Save

This is money for goals within the next few years.

Examples:

- Education funds

- Travel savings

- Car replacement

- Home-related expenses

Safety and stability are usually more important here than growth.

3. Money to Grow

This is money intended for long-term wealth building.

Examples:

- Stocks

- ETFs

- Mutual funds

- Retirement investments

This category involves more risk, but also greater long-term growth potential.

The important point is:

Only invest money you won’t immediately need.

Understanding Risk Visually

One reason investing feels scary is because risk feels invisible.

But risk becomes easier to manage when you can actually see it.

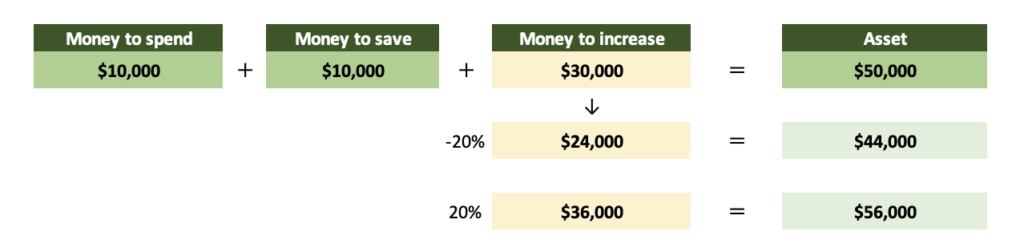

For example, imagine your investments temporarily decrease by 20%.

Would your daily life still feel stable?

Now imagine your investments increase by 20%.

How would that affect your future goals?

Thinking this way helps you determine:

- how much risk feels emotionally comfortable,

- and whether your current asset allocation matches your lifestyle.

Asset Allocation Is Personal

There is no perfect allocation for everyone.

Your balance depends on:

- Age

- Income stability

- Family situation

- Future goals

- Personality

- Risk tolerance

Some people value stability.

Others prioritize growth.

Both are valid.

The goal is not to copy someone else’s financial strategy.

The goal is to create a system that supports your life.

Financial Anxiety Often Comes From “Not Knowing”

Many people believe money anxiety comes from not having enough money.

But often, the bigger problem is:

Not being able to clearly see what is happening financially.

When your money becomes visible:

- decisions become easier,

- spending becomes more intentional,

- and the future feels less overwhelming.

That’s why visualization matters so much.

Start Simple

You do not need to become an investment expert overnight.

You only need to begin by understanding:

- what you own,

- what you owe,

- what you spend,

- and what your money is meant to do.

Small clarity creates long-term confidence.

Free Download

The original article also introduces a downloadable asset management sheet designed to help visualize:

- spending money,

- savings money,

- investment money,

- and risk balance.

Using visual tools can make asset management feel much easier — especially for beginners who struggle with financial anxiety or organization.